Health Insurance - What To Know?

If you want to follow a literate focus and elite target for health insurance, you must become acquainted with healthcare cost management. To accomplish this capacity to apply healthcare management, you need to be able to properly compare and contrast the difference between individual and group health alternatives. You also need to differentiate between the concept or the format of receiving health insurance under a fee-for-service model or a managed care health plan model.

Looking into your relationship with health insurance, you need to have the capacity to incorporate health costs during your retirement and measure this cost's effect in your retirement plan. To make the proper assessment of the situation, you need to consider your financial resources, your existing, and your future coverage, both under your individual or group plan and on your Medicare coverage once you retire. Additionally, you must understand the difference and the impact of acquiring health coverage using COBRA or considering the Medicaid options in health insurance.

With health insurance, we have something exciting because, with the passage of the Affordable Care Act, there has been a substantial change in the way we interact with health care management. Because of the Affordable Care Act's dramatic impact, all the parameters and principles we need to consider when purchasing health insurance have changed. I have always argued that a financial product's complexity is associated with the number of moving parts that a financial product has. Health insurance is the most complex financial product because you do not have any other financial product with more moving parts. Health insurance is a sack of multiple options. All these different options where you pay the insurance company a certain amount of money, basically you are protecting yourself from the possibility of some conditional, some situation developing and you having to incur some expenses. If that is the case and that situation ends up happening, you can pay the agreed price for that specific condition based on the contract you have signed with the insurance company. That is why I call a health insurance policy a sack of options.

The passage of the Affordable Care Act divided the world of health insurance into two sub-worlds. On the one side, you have the world of no subsidies, and on the other side, you have the world of subsidies. Depending on several specific situations for you and your family, you can belong to the world of subsidies or the world of no subsidies. Within the world of subsidies, if you qualify, then you can decide if you want to take them or not. It is your prerogative to take the subsidies if you qualify for them. You are not obligated to take the subsidies, but you would take the amount of help you get from the federal government in most instances. On the other hand, if you don't qualify for the world of subsidies, you can purchase health insurance in the world of no subsidies and would not be getting any help from the federal government to pay for health insurance costs.

Insurance companies have created all these different products in the world of subsidies and no subsidies. ACA was the genesis for the so-called call metallic products. The actual names are bronze, silver, gold, and platinum plans, and the difference has to do with the amount of cost-sharing that the end-user is obligated to incur. Depending on your income level and on your plan selection, you will qualify for a substantial amount of subsidy provided by the federal government that will pay for a significant part of your health care insurance costs.

In the bronze plan, you have what they call 60/40 sharing, so that means you pay for 40% of the cost-sharing element, and the insurance company pays the other 60% of all expenses up to a yearly cap that the federal government defines. In the silver plan, you go to a 70/30-type of sharing structure, and then in the gold plan, it is 80/20, and in the platinum, the plan is 90/10.

If you move to the other side of the line to the world of no subsidies, there is no help there. You have multiple portfolios of products that you can use in the world of no subsidies, and you have what they call short-term medical insurance, which is not short-term anymore. In the past, short-term insurance would be limited to coverage for less than a year. Today, you have short-term medical insurance that can last up to three years. The name is the only thing that is still there because everything else is not short-term medical insurance.

There is a series of supplemental health insurance products that you can purchase to take care of almost any health care risk in the world of no subsidies.

Essential Health Benefits (EHB)

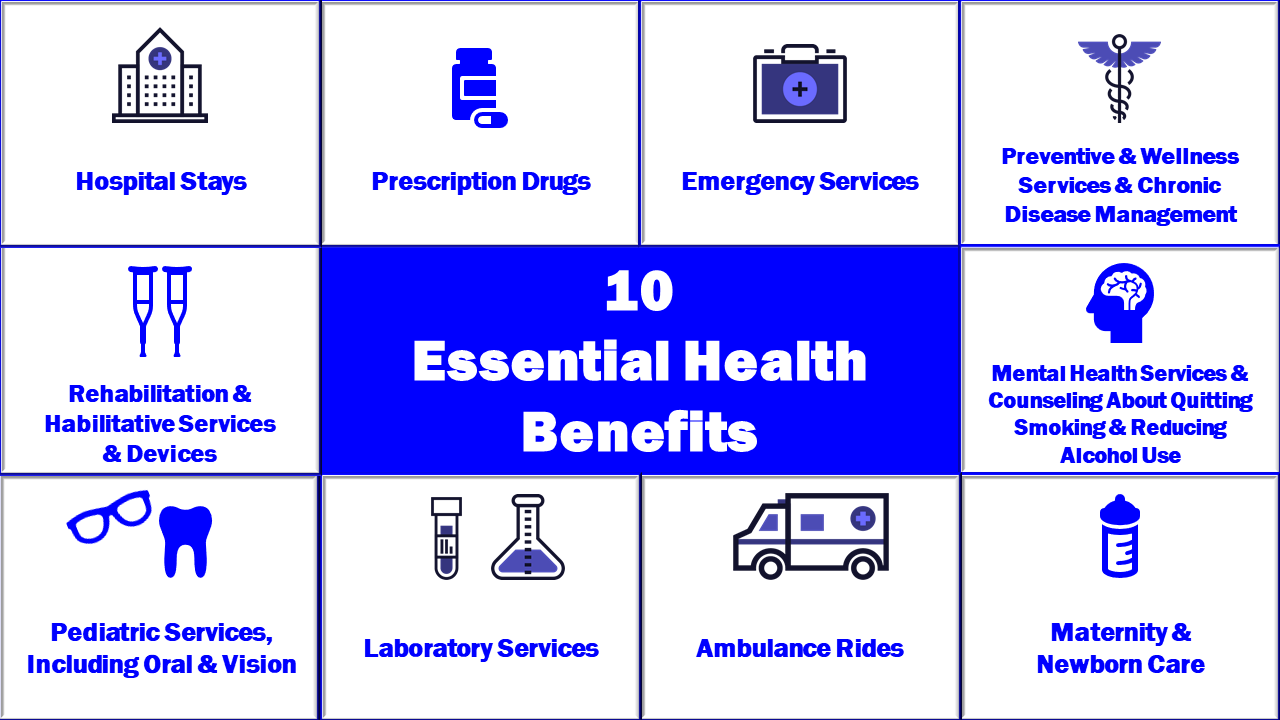

It is imperative that for any product to be on the world of subsidies created by the Affordable Care Act, the product needs to satisfy an extensive list of requirements. Many of these requirements make these products very expensive. One of them is the concept of the Essential Health Benefit. With the passing of the Affordable Care Act law, the government decided to build these very comprehensive health insurance plans that would cover an individual and their family for the totality of the possible health situation that could occur. And what they ended up doing is they ended up creating these complex products that are full of benefits but are also at the same time very inefficient and expensive. There are many instances where an individual or a family does not need different coverage types imposed on them with these essential health benefits. The EHB concept comprised a list of 10 areas of coverage, including maternity care, rehabilitative services, pediatric services, mental and behavioral health treatments, preventive services, hospitalization, laboratory services, prescription drugs, ambulatory patient services, and emergency services.

You cannot take any one of these services out. For example, if you are a 64-year-old male married to a 64-year-old woman, you definitely would not be considering purchasing pediatric services coverage. Still, you do have to include that coverage because you cannot take that benefit away from the policy. The same principle will apply, for example, to maternity care. No matter that you will not have any kids, you are obligated to purchase and pay for these essential health benefits. That makes some of the Affordable Care Act's products so inefficient because they would not be pertinent to many people. It becomes costly and not outfitted with the capacity to be tailored to individual situations.

The government tried to make the products more affordable, so we started getting all these different health coverage levels, adding another level of complexity for these products. There is this fight within the political parties in which the Democrat party wanted Medicaid to help individuals through 100% of the FPLC. Coverage under the Affordable Care Act would start at 100% of the FPLC level. The federal government helps individuals with some subsidy level between 100% and 400% of the federal poverty level chart. This tug of war never settled, and what we ended up with was the situation where somebody with a higher level of income would get more subsidies than somebody with a lower level of income; This is something that nobody could fully understand, and it did not make any sense at all.

We used to approach the concept of analyzing risk substantially differently. It has changed based on the fact that there are no pre-existing conditions associated with these products; Additionally, the level of subsidy completely distorted anything that had to do with the product's financial structure. ACA and now ARPA eliminated all financial analysis and health considerations, so the rules and concepts you would apply to obtain the product changed substantially.

The Networks

Within health care management, you have these network structures that are fundamental in lowering the product's cost. Suppose you have an HMO provider, a health maintenance organization provider. In that case, insurance companies can control expenses by making sure that you have a primary care physician and making sure you have a well-defined network. You buy a health insurance plan under an HMO network structure, and you need to make sure you go to the assigned or the selected primary care physician and stay within the network. When you follow that format, you will be getting health care in the most economical way possible. It is a strictly controlled system, but at the same time, very efficient in terms of the way you manage your health care costs. Suppose you select a Preferred Provider Organization (PPO) type of network. In that case, you have this plan that is more flexible, more open, and you don't need to have a primary care physician, and under that format, then you have more freedom, you can go to more doctors and more hospitals and medical facilities. But at the same time, you end up paying more money. Depending on the type of network structure you selected in your plan, you would have more costs, fewer costs, and more freedom.

Unfortunately, some insurance carriers started running into financial difficulties because of the adjustments they had to do through health care management, then decided to limit some of these networks.

We ended up with limitations in the marketplace, and basically, we ended up with only HMOs or EPOs. You do not have PPOs, so you have a very restricted network that you need to use. That created problems for a lot of people. We want to emphasize that you need to make sure that you understand the network concept whenever purchasing health insurance. And you need to make sure that you know who your primary care physician is, what type of network you have, and all aspects associated with the way health care is provided to you.

Before the ACA, policy duration was open. With the ACA, the contract duration is now one year, so every 12 months, you get an opportunity to decide on a different insurance company, cost structure, or network.

The Cost Structure

It is critical to understand the cost structure of a health insurance plan because this will define many aspects of how you're going to use your policy. We have five cost structure elements in the health insurance plans. The five elements are:

- The monthly premium, the amount of money you pay monthly to have your health insurance.

- The deductible. The best way to understand it is the amount of money you do not have health insurance. If you have a $4,000 deductible, that means that for the first $4,000 of health care expenses, you have to pay the money from your pocket, and you don't have insurance until you reach that deductible.

- After you reach your deductible, you will start "sharing" with insurance companies on a predefined specific percentage of the cost associated with health care. For example, you can have an 80/20 coinsurance structure or a 70/30 coinsurance structure, and what that means if you have 80/20 means that the insurance company would pay for 80% of the expenses. You will end up paying for 20% of the expenses up to a limit defined by the federal government.

- The copayment is a fixed amount of money that you pay for certain services. You have a $40 copayment to see a primary care physician or a $70 copayment to see a specialist, constituting a fixed amount of money you pay every time you use certain services.

- Finally, you have what they call the maximum out of pocket, which is a quantity, as the name implies, the maximum amount of money that would be coming out of your pocket by the end of the year. This is your total exposure amount, representing the maximum amount of financial exposure or the amount of money you have at risk based on that specific plan you purchased.

Again, you have five cost elements: Premium, deductible, coinsurance, copayment, and the maximum out of pocket. The way you set up each one of these elements will affect your cash flow substantially and the total expenditures you will incur based on whatever happens.

In terms of which product is better, there is no good or bad product because it is always associated with what ends up happening. If you decide that you want to take a lot of risks, so you select a bronze plan and buy a product where you pay a meager premium, but it turns out that you end up using the system more than expected, you pay a lot of money. If nothing happens to you during the year, you have saved yourself a substantial amount of money. On the other hand, if you get in an accident or get ill, that is the most expensive way for you to have health insurance.

If you decide that you want to pay a lot of money upfront, but nothing happens to you during the year, then basically, you have wasted a lot of that money because nothing happened to you. You were paying some costly monthly premiums for your health insurance. The point is that there is no excellent or flawed product. It all depends, and it's all associated with actually what ends up happening, and in many instances, sickness or accidents are not predictable. But what you can do is, if you are in good health and have a very moderate lifestyle, you could take some risks. But if you are sick, you should get into a product with more up-front payments and make sure that you pay the least amount for them whenever you incur the anticipated expenses.

How The Federal Government Helps With Expenses

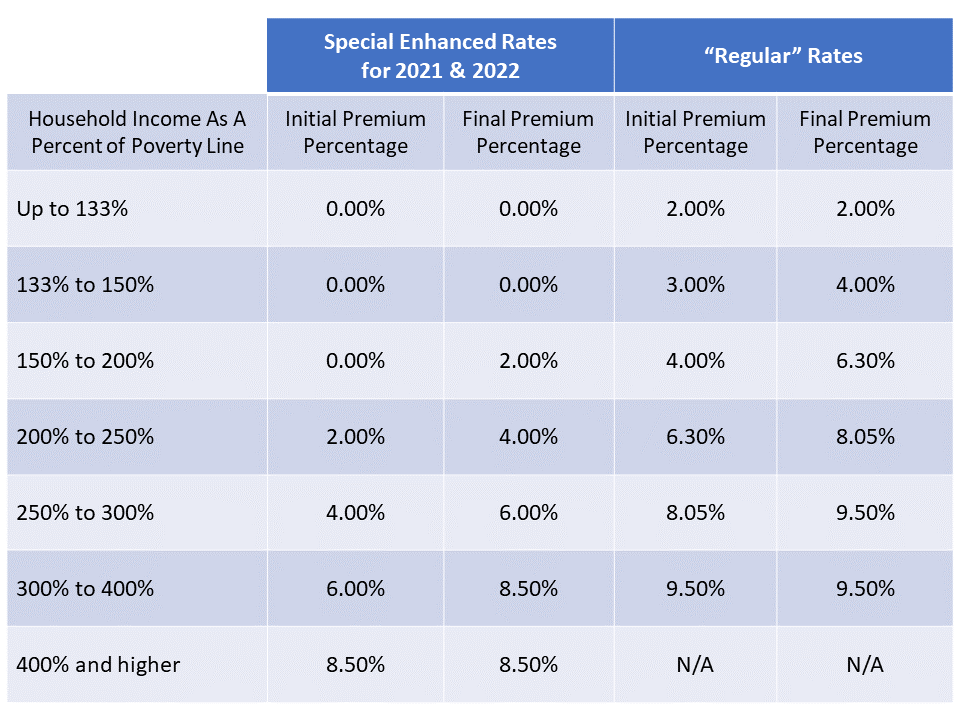

(Amount Taxpayers Must Spend on Policies Purchased Through State-Run Health Insurance Exchanges To Qualify for Premium Assistance Tax Credits)

The federal government helps you pay for health care costs in two distinct ways.

The Federal government can help you pay for your monthly premium. They do that through the Advanced Premium Tax Credit (APTC). Uncle Sam will pay for the totality or for a substantial portion of the monthly premium you need to pay for your coverage for you and your family. That is the first way the Federal government helps you.

The second one is called cost-sharing. You have all these different components that we mentioned before regarding a health insurance plan's cost structure. You have cost-sharing. There are certain events where you share the cost with the insurance company. Again, the Federal government can help you with cost shedding based on your level of income.

The way this works is straightforward. Every year the Federal government comes out with this "poverty" chart. The Federal government defines every year this imaginary line that is at 100% of FPL.

What they say is that anybody that is under 100% FPL is considered poor. Everybody to the right of 100 % FPLC will receive some help to pay for their monthly premium health insurance. The amount of subsidy you are getting depends on where the level of income you and each wage earner in your household declare in your family income tax forms. Uncle Sam takes into consideration the totality of the household income for all the members of your family. They come up with the total amount of money that your family receives. Based on that, they see where you fall within the FPL chart and calculate a certain amount of subsidy. If your household income level is less than 300% of the FPLC, you will get help for everything that has to do with the monthly premiums and cost-sharing. If it is over 300 % of FPL, you will get help with monthly premiums but no cost-sharing.

It is essential to mention that the American Rescue Plan Act signed into law on March 11, 2021, modifies these figures, and provides additional help for individuals beyond 300 % of FPL.

In terms of cost-sharing, if you make between 100 % and 150 % of FPL, you will get subsidies for up to 94% of the actuarial value of the health care costs if you enroll in a Silver plan. If you make up to 200% of FPL, you get 87% of the actuarial value when enrolled in a Silver plan. If you make up to 250% of FPL, you get subsidies and help for up to 73% of the actuarial value in a Silver plan. In terms of the monthly premium, if you make up to 400% of FPL, you will qualify for some level of help for your monthly premium.

Under the Affordable Care Act, and now under the American Rescue Plan Act (ARPA), the Federal government does provide a substantial amount of money for individuals to help them with the health care costs. There is a substantial reduction in the amount of money they need to pay for healthcare for individuals who make less income. For those individuals that do not qualify for any subsidy, the cost associated with health care grew up exponentially. Today, it is costly to own one of these products if you are not getting any subsidy from the Federal government. That has created some serious problems. ARPA does modify the subsidy level for the affluent, allowing more Americans to receive the federal subsidies' benefits.

Whenever you are going to buy health insurance, you can do it in many different ways. You can go directly to the marketplace and get it there, the marketplace that the Federal government created for that. Or you can use an insurance agent that can help you with the process.

My recommendation is to use a seasoned and knowledgeable insurance agent that knows everything that has to do with and how to apply and maximize the levels of subsidies you can get.

You must understand the totality of the package that you are getting. It's also imperative that you understand the network concept that I mentioned before because if you don't know to use that, you can make some errors that come through very expensive for you.

The ownership dimension is encapsulated within a minimal number of possibilities for who can participate in the program or can have the product's benefits. The fundamental nucleus of health insurance is around the family, and the definition of family exclusively limits the people that can participate in the program. You can either include everybody in your family or exclude some of the family members. From the instant the Affordable Care Act was passed, the family for health insurance is related directly to the individuals in your income tax declaration. Because of that limitation associated with who can participate in the plan, the ownership dimension is subordinate to health insurance. The risk of return dimension will control or determine the outcome you're going to have in the relationship between your money and the health insurance product.

Health insurance is about making sure that you are very much aware of the exact characteristics of the plan that you register for and to make sure that you maximize the benefits that you get within the program because of these superior powers of risk and return on health insurance, the R dimension is dominant. If you have the right product, you will have limited exposure to costs associated with health care management, but if you don't have the right product or you don't understand the product that you have, or you don't have health insurance, the financial exposure that you're going to be having can make you go bankrupt. Another fundamental element in health insurance has to do with the amount of subsidy you might be entitled to base on your income levels and the number of people in your household.

Because of these, the tax dimension is also dominant in health insurance. Suppose you are qualified as an affluent individual, somebody with more than 400% of the federal poverty level chart. In that case, the tax dimension is essential, but now it would have to do with how you use standard deductions or itemizations when you do your taxes. But because of all the influence that taxes have on health insurance, the tax dimension is dominant. The time dimension lost part of its importance with health insurance because you have the opportunity to revise your plan every year. Additionally, because of the lack of pre-existence within the product, then every year, you have the chance to revise everything and correct any errors you have made in terms of what you have selected. Because of these, the time dimension is subordinate in health insurance.